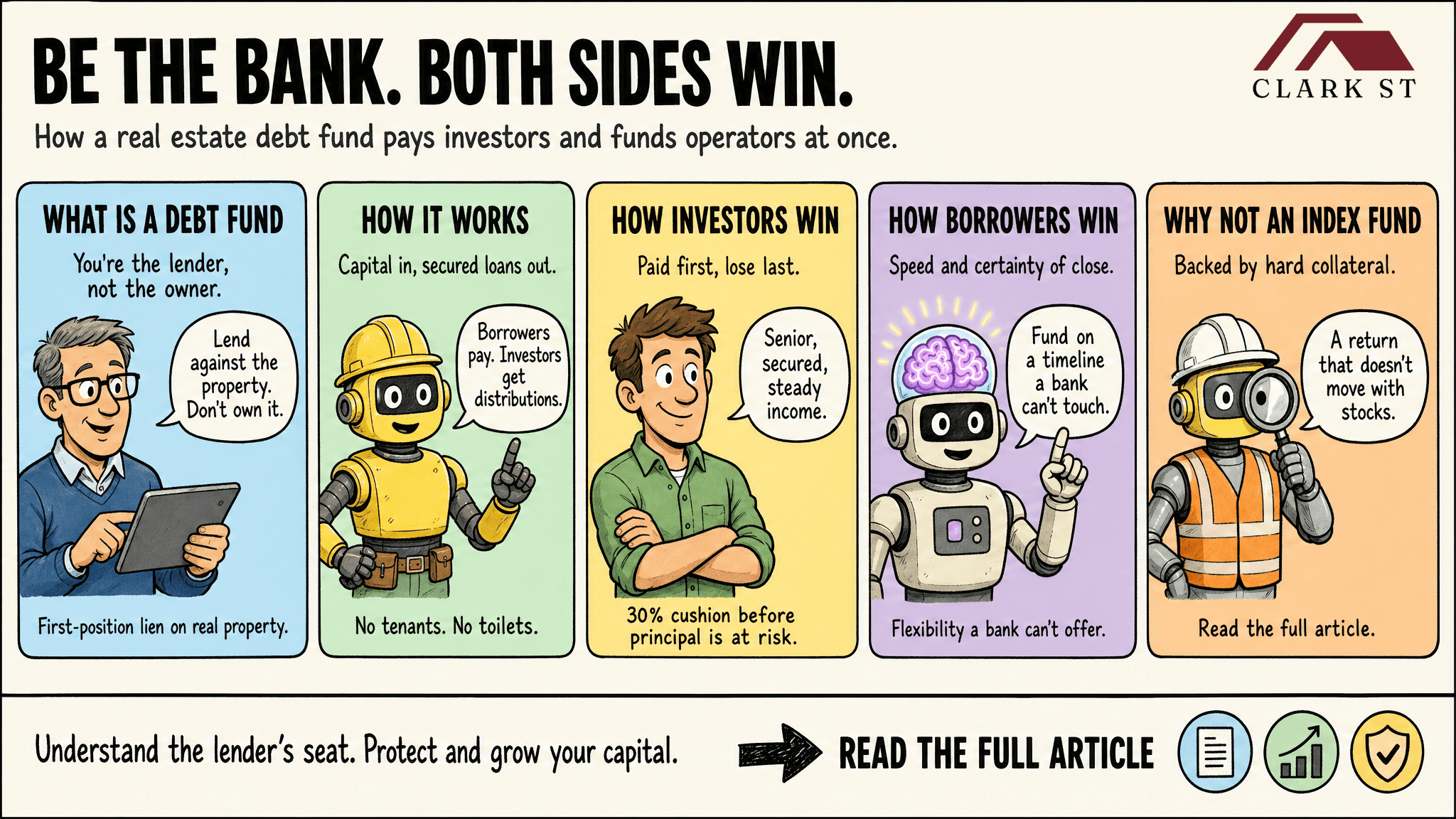

A real estate debt fund lends money to real estate operators and holds a first-position lien on the property as collateral. You're the bank, not the owner. When the borrower performs, you collect interest. If the borrower defaults, the fund can (and will) foreclose and recover from the property itself. That lender position is the whole ballgame and it's what makes a debt fund behave differently from an equity deal.

I spent years as the operator who used this type of leverage, before I accepted a dime of anyone else's money. I've also invested as a limited partner. Both seats taught me the same thing. A good debt fund is one of the few places in real estate where both sides of the table win at once. The investor gets a secured, passive position. The borrower gets capital a bank could not move fast enough to provide. That double-sided win is the reason we like providing debt in this current real estate market.

TL;DR

- A real estate debt fund pools investor capital and lends it to well-vetted operators, secured by a first-position lien on real property.

- You hold the lender position. You sit ahead of the equity owners and the property backs the loan.

- Investors win on a passive, secured position with a predictable income role in a portfolio.

- Borrowers win on speed, certainty of close and flexibility a bank cannot offer.

- It's built for the investor who values steady income and capital protection over a big swing.

What is a real estate debt fund?

The first millionaire of California's mid-1800s gold rush was a man named Samuel Brannan. Samuel didn't strike gold. He didn't even try. He sold the picks and shovels to the 49ers chasing their fortunes in the hills. Samuel didn't know where to find the gold, but he knew the miners would definitely need equipment to go dig for it.

A real estate debt fund takes the same approach.

The fund is a pool of investor capital that makes loans to real estate operators (the picks and shovels), with each loan secured by a lien on the property (the gold).

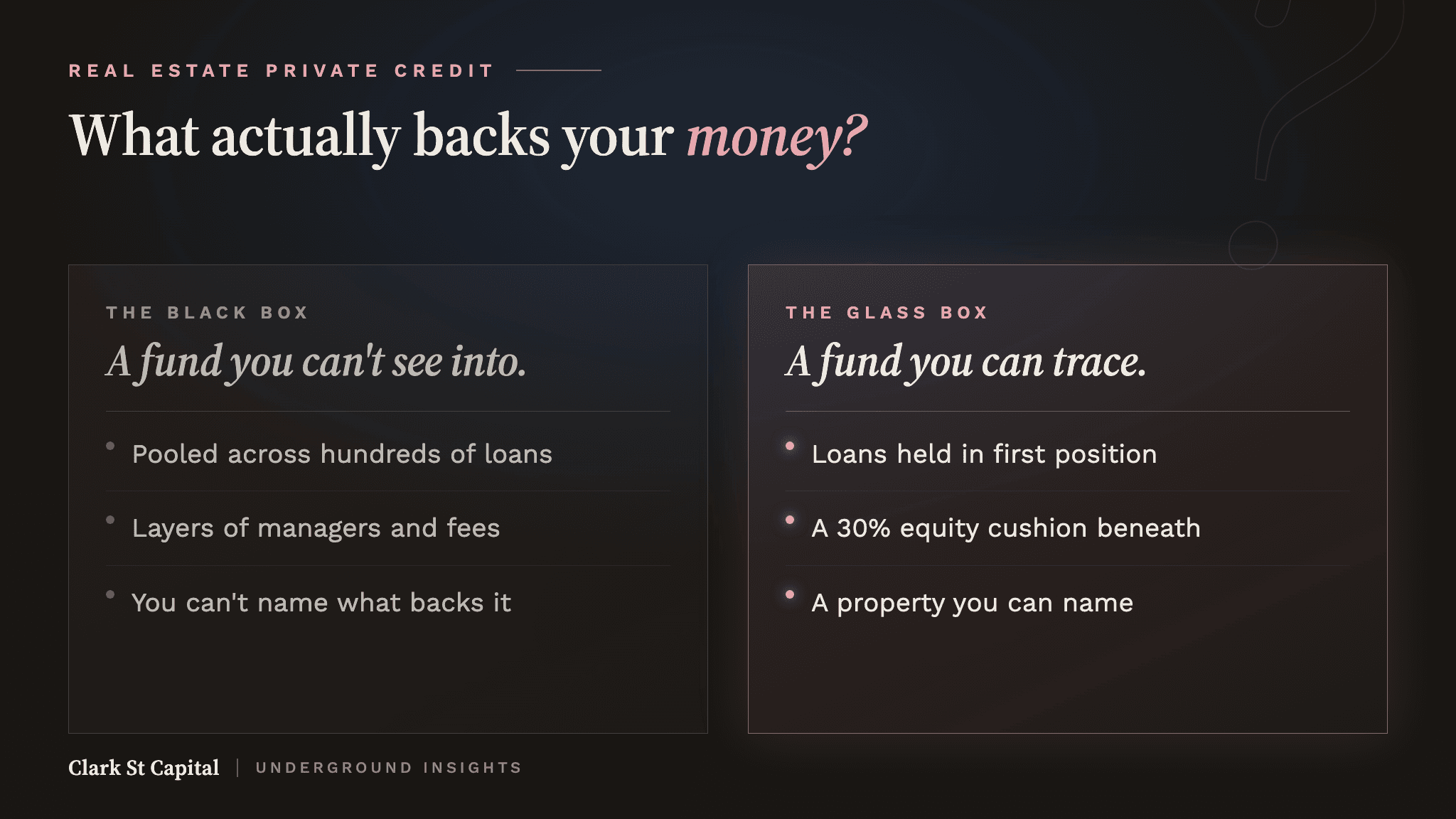

In a debt fund, you're not buying a building. You're lending against one. In fact, you're lending against many. You're the lender in first position, the same seat a bank sits in and the property is your collateral. When the borrower pays, you earn interest. If the borrower stops paying, the fund has a legal claim on the property and can foreclose to recover its capital.

That is the line between debt and equity. Equity owns the asset and chases its appreciation. Debt lends against the asset and collects interest. A debt fund makes money when the borrower pays the note, not when the building goes up in value. Two very different machines.

How does a real estate debt fund work?

The fund raises capital from investors. This pooled capital comes in, secured loans go out to vetted real estate operators who need financing: a flipper buying a property, a builder funding a development project, a sponsor bridging between purchase and permanent financing.

Borrowers make their payments to the fund. The fund collects, covers its costs and passes income through to investors as distributions. No tenants. No toilets. No contractor who ghosted you in month four. The fund manages the loans, the paperwork and the workouts if a loan goes sideways. You hold a position in a diversified pool of secured loans and let the manager run it. Every loan is secured by a first-position lien on the property. That's the engine.

Pooling is the point. A single loan to a single borrower is concentrated risk. Spread the capital across many loans and many borrowers and no one bad loan sinks the whole position.

Want to learn more? Ed walked through how a debt fund works on Real Estate Underground, Episode 168.

How do investors win in a debt fund?

It's a simple equation. The debt fund gets paid first and it loses money last.

A debt fund is a secured, senior position, run across a concentrated and diverse pool of properties, which throws off steady income.

Your loan is backed by a lien on real property and sits ahead of the equity, so the owners absorb losses before the debt fund capital is ever affected. That's not a promise of safety. It's where you sit in line.

A debt fund is genuinely hands-off for the investor. You're not vetting contractors, walking buildings or managing a refinance. The manager underwrites the loans and handles the problems. You vet the manager once, rigorously, then let the model work.

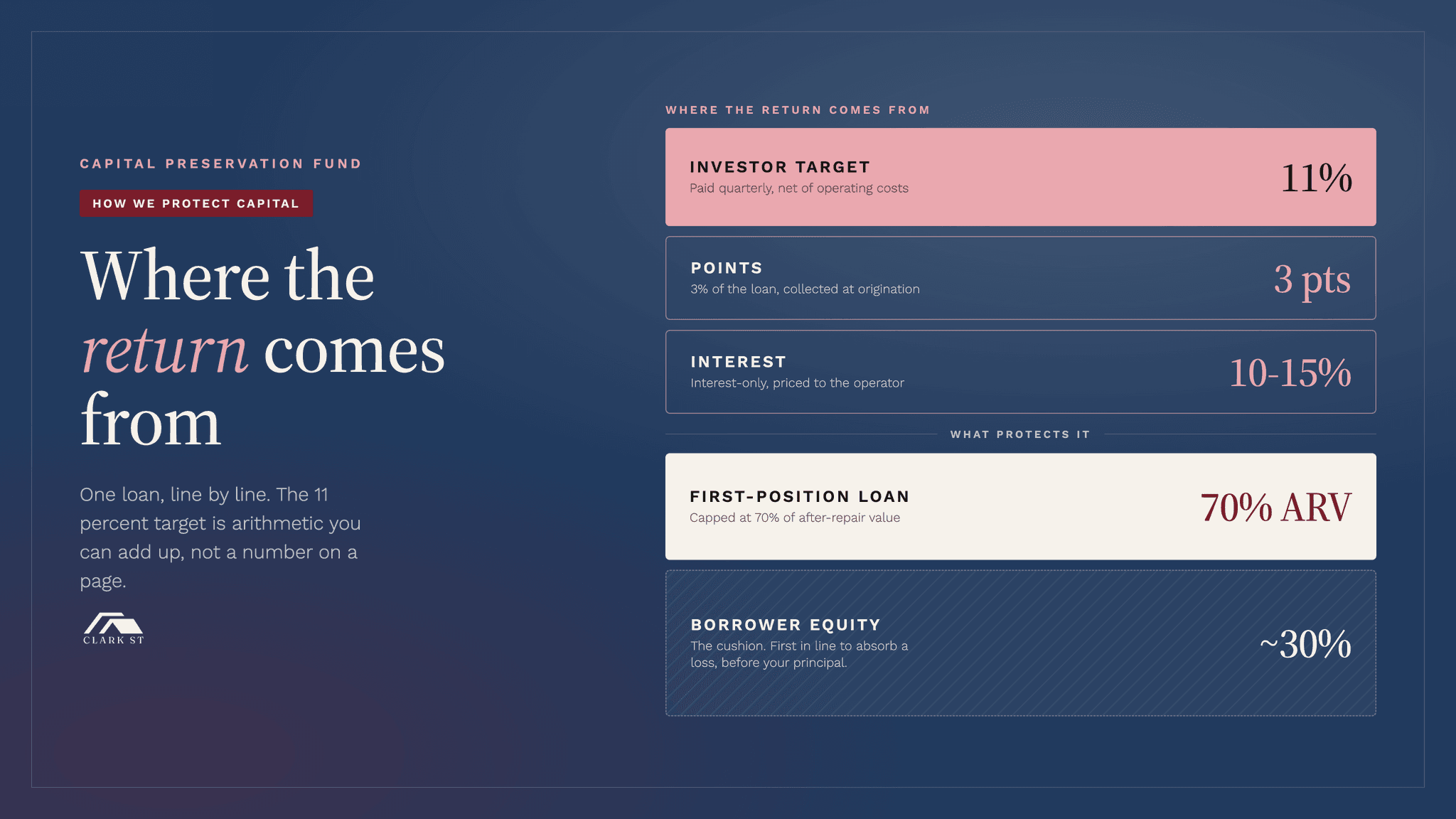

The fund's loans are written at 10%-12% interest plus 3 points (depending on the project), secured by a first-position lien. That is what a borrower pays for speed and certainty. It's where your distributions come from, after fund costs. Your exact net return depends on the fund and the loans it holds. Keep in mind, any real estate investment carries risk of loss.

Let me show you how we manage the downside to protect our investors first.

Picture a property worth $570,000. The fund lends $400,000 against it, around 70% of value. The borrower brings $170,000 as a downpayment. That equity sits behind our loan. Values would have to fall 30% before your principal is even at risk. The borrower loses their money before the investor loses a penny. The borrower has also pledged a personal guarantee. So even if the property loses 30%, the fund still has recourse. That cushion, plus the first-position lien, plus the personal guarantee is what "secured" actually means. You're sitting in front of the borrower's cash and assets.

That is the role debt plays in a portfolio: steady income and capital protection. We're swinging for singles and doubles, not home runs. Equity is the home-run swing. There's a place for that in your real estate portfolio, but there's inherent risk in it. Debt is the steady single. If you already hold equity real estate, a debt position balances it.

How do borrowers win in a debt fund?

Borrowers win on speed, certainty of close, flexibility and speed-of-service a bank can't offer, from a lender who actually understands real estate and has sat in both seats as the borrower and the bank.

This is the other half of the story most investor content skips. It's the half that makes a debt fund work. A fund only earns the investor's interest if good borrowers want to borrow from it.

Speed. A bank can take weeks or months to underwrite a real estate loan, if it does the loan at all. An operator with a property under contract does not have months. A debt fund built to move can fund on a timeline a bank cannot touch. For a flipper or a builder, that speed is the difference between getting the deal and losing it.

Certainty of close. A bank loan can fall apart late, on a committee decision or a fresh appraisal or a policy that changed mid-process. A debt fund that did its underwriting up front gives a borrower real confidence the money will be there on closing day. Certainty is worth paying for, and good operators know it.

Flexibility and speed-of-service. Banks lend inside narrow boxes. A property that needs work, an unusual structure, a project between phases: a debt fund can structure the loan around the actual deal instead of forcing it into a template. And as the project plan executes, the debt fund can service support the borrower with speedy renovation reimbursements, their own vendor network and strategic advice from 15+ years in the value-added real estate business.

A lender who understands real estate. A bank loan officer reads a file. An operator-run fund analyzes the deal from a flipper's perspective. When the lender has bought, fixed, financed and sold real estate, they know which questions matter and where a project tends to go sideways. That makes them faster to a yes on a good deal and even faster to a no on a bad one. The same operator judgment that wins the borrower is what protects the investor's capital.

That is the two-sided win. The borrower gets capital they could not get fast enough anywhere else. The investor gets diversified across a set of well-secured loans to vetted borrowers on real assets.

The honest objection: why not just buy an index fund?

Fair question and I get it often. Index funds are liquid, cheap and you do not have to trust an operator. A private debt fund is none of those things. Your capital is committed. There are real costs and you're betting on the manager's underwriting.

What you're buying instead is a return stream that does not move in lockstep with the stock market and a position secured by hard collateral. An index fund is a claim on a basket of companies. A debt fund position is a claim backed by a lien on real property. For most people who've built real wealth, the answer is not one or the other. It is using each for what it does well.

How Clark St thinks about lending

I spent more than two decades building systems before I went full time in real estate. That taught me to operationalize our systems to make these decisions the same way every time. On the lending side that means the same underwriting questions on every loan and a plan for the loan that goes bad before we ever fund the one that looks great.

We've been the borrower. We've closed on a clock, needed certainty and wanted a lender who understood the deal instead of just the file. That's exactly the lender we aim to be on the other side of the table through the Clark St Capital Preservation Fund, our first debt fund, live today. Knowing both seats is what informs us what a careful lender should be checking before the wire ever goes out.

FAQ

What is a real estate debt fund? A real estate debt fund pools investor capital and lends it to well-vetted real estate operators, with each loan secured by a first-position lien on the property. Investors earn returns from the interest borrowers pay. The property and the borrower's personal guarantee back the loan if a borrower defaults.

How does a real estate debt fund work? The fund pools capital from investors and makes secured loans to operators. Borrowers pay interest, the fund collects, covers its costs and income flows back to investors as distributions. Investors hold a passive position in a diversified pool of secured loans.

How do investors make money in a real estate debt fund? Investors earn income from the interest borrowers pay on the loans. The position is secured by a lien on real property and sits senior to the equity owners, which is the structural reason debt is the safer seat. Returns vary by fund and deal. Please remember, every real estate investment carries risk of loss.

Why would a borrower use a debt fund instead of a bank? Speed, certainty of close, flexibility and speed-of-service. A debt fund can fund faster than a bank, give a borrower confidence the money will be there on closing day and structure a loan around the actual project.

Who should consider a real estate debt fund? Accredited investors who want steady income and capital protection more than the uncapped upside of an equity deal. It is often a good first position for a busy professional who wants real estate exposure without owning or operating property.

Want the operator's read on private credit?

I send the same lessons I would give a friend over coffee, real deals, what worked and what did not, in the Clark St Underground Insights newsletter. No hype, no pitch, just how an operator thinks about protecting and deploying capital. If you want to understand private real estate debt before you ever consider putting a dollar to work, join the list.

Want to listen in on Ed's conversations with operators across the country? Subscribe to the Real Estate Underground podcast.

About Ed Mathews

Ed is the founder of Clark St Capital, Clark St Homes and Elevista. He started investing in 2011 after analyzing deal after deal and making zero offers, until a mentor handed him a pen and made him sign his first contract. Since then, Clark St has operated across single-family, multifamily and land development, with Ed also invested as a limited partner in funds and large multifamily projects. Ed also spent more than two decades in Silicon Valley building systems for global companies. He hosts the Real Estate Underground podcast.