TL;DR

- "Non-recourse" agency debt contains bad-boy carveouts that flip the loan to full personal recourse against the sponsor.

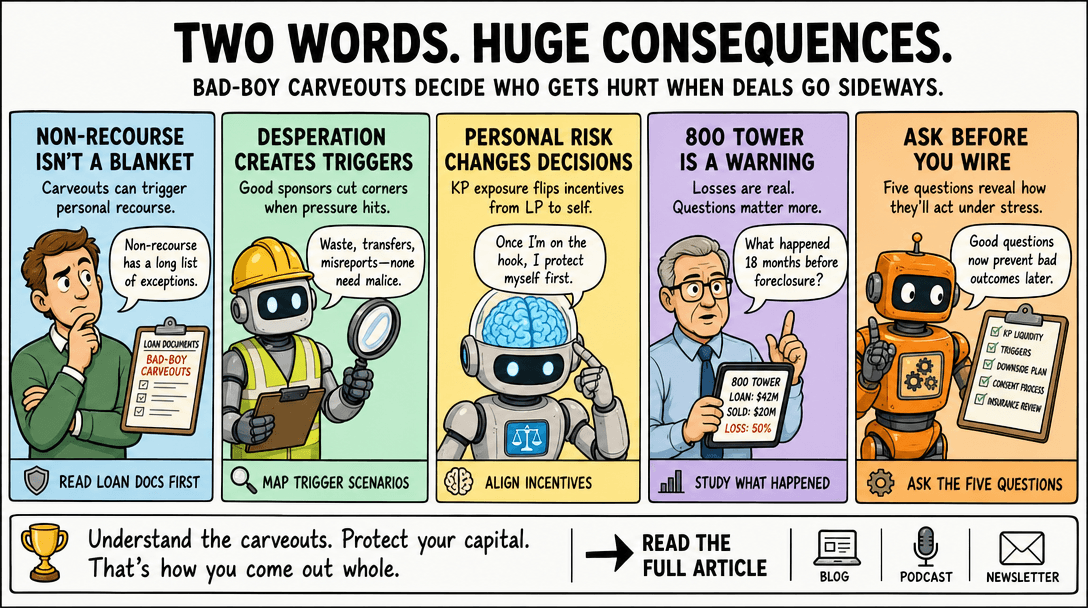

- The triggers almost never require malice. They require desperation.

- A sponsor with personal recourse on the line stops optimizing for LP recovery and starts optimizing for their own survival.

- Five questions every LP should ask before wiring into a deal in this cycle.

The two words that decide whether a sponsor protects your capital or their own interests when a deal goes sideways.

I've had the same conversation a dozen times in the last six months. Smart LP, second or third syndication, did the homework on the sponsor and the market. They wire in. They never ask one question.

"Do you know what triggers personal recourse on this loan?"

The answer is almost always no. They assumed "non-recourse" meant the GP couldn't lose more than the equity they'd put in. That's what the marketing deck said. That's what the sponsor told them on the call.

That's not what the loan documents said.

What "non-recourse" actually means

Agency debt from Fannie and Freddie is technically non-recourse. The lender's primary remedy if things go sideways is the property. They foreclose, sell, and the sponsor's personal balance sheet stays out of it.

That's the headline. The fine print is a section called bad-boy carveouts.

Carveouts are specific behaviors that flip the loan from non-recourse to full personal recourse against the Key Principal. The sponsor signs them at closing. The lender sleeps better. And most LPs never read them.

The list is longer than you'd think. Waste, which means intentionally letting the property deteriorate or diverting cash away from maintenance and debt service. Unauthorized transfers, meaning selling or transferring interests without lender consent. Environmental hazards where the sponsor lacks the liquidity to remediate. Fraud or misrepresentation, which includes any reporting error across the life of the loan.

Read that list again. Notice something? Almost none of those triggers require malice. They require desperation.

How a good sponsor becomes a bad one

Here's the scenario nobody underwrites for.

Your sponsor bought a property in 2022 on a floating-rate bridge loan. The pro forma assumed a refinance into permanent debt at month 30. Rates moved against them. Insurance tripled. Two anchor employers in the workforce housing comp set went dark and rents softened.

The DSCR is now 1.05. The rate cap expires in six months. The refi isn't there.

What does a sponsor in that position do?

If they're disciplined, they call the LPs, mark the equity down, and start the workout. If they're desperate, they start cutting corners. They defer maintenance to preserve cash. That's waste. They quietly move an LP interest to a friendly capital source without lender consent to plug a hole. That's an unauthorized transfer. They lean on the property manager to fudge an occupancy number on the monthly report so the DSCR covenant doesn't trip. That's misrepresentation.

Each one of those decisions, made by a sponsor trying to save the deal, flips the loan to full recourse against their personal balance sheet.

Here's the part LPs miss. When the sponsor's balance sheet is suddenly on the line, every subsequent decision gets made through that lens. They're no longer optimizing for LP recovery. They're optimizing for their own survival.

That's how a good sponsor becomes a bad one. Not character. Math.

Ed unpacked this exact dynamic with a workout attorney on a recent episode of Real Estate Underground. Worth the listen if you want to hear what these conversations sound like from the lender's side of the table.

The 800 Tower lesson

Louisville's 800 Tower is the case study sitting on every institutional desk right now. $17 million in renovations. Luxury amenities. A $42 million loan. Fannie Mae foreclosed and sold it for just over $20 million. A 50% loss on the loan, equity wiped.

The interesting question isn't how the deal failed. The interesting question is what the sponsor was doing in the eighteen months before the foreclosure. Were the carveout triggers clean the whole way down? Or did the sponsor, watching their equity evaporate, make decisions that exposed them personally?

I don't know the answer on 800 Tower. I do know that across the wave of distress coming through 2026, that question is going to determine which sponsors come back to do another deal and which ones don't.

What you can actually ask

The carveout structure is one of the cleanest signals of how a sponsor will behave under pressure. If they understand it cold, they've thought about the downside. If they get fuzzy, they haven't.

Five questions worth asking before you wire:

-

Who is the Key Principal on the loan, and what is their personal liquid net worth relative to the carveout exposure? A KP with $500K in liquidity guaranteeing carveouts on a $30M loan is a problem. Their incentive under pressure is not the same as a KP with $5M.

-

Walk me through the specific carveout triggers in the loan documents. Not the marketing summary. The actual triggers. If they can't, that's the answer.

-

In the downside case where DSCR drops below 1.0, what's the operating plan, and which decisions could expose the KP personally? Listen for whether they've mapped this. Most haven't.

-

What's the lender consent process for transfers, and what happens if you need emergency capital? This is where unauthorized transfers happen. If the answer is hand-wavy, the risk is real.

-

Show me the insurance covenants in the loan documents and the current policy side by side. A coverage gap is a default trigger. Most sponsors haven't reconciled these in 24 months.

How we handle it at Clark St

We read the loan documents before we read the pitch deck. Every deal. Every time.

We do it because we've watched what happens when sponsors don't, and because the carveout structure tells us more about how a deal will perform in distress than any pro forma ever will. We document the KP exposure, map the trigger scenarios, and stress-test the operating plan against them before capital ever moves.

The 2026 environment will separate sponsors who understood their downside from sponsors who didn't. The LPs who come out of this cycle whole are the ones asking these questions now, before they wire, instead of learning the answers in a workout call eighteen months from now.

Non-recourse is a word in a marketing deck. Bad-boy carveouts are the actual contract. Know the difference before you fund.

Get the underground intel. Clark St Underground Insights is the newsletter Ed writes for LPs who want story-driven lessons from inside the deals, not generic market commentary. One email, no fluff, every other week. Subscribe here.

Listen to Real Estate Underground wherever you get your podcasts. Real Estate Underground podcast.

About Ed Mathews

Ed is the founder of Clark St Capital, Clark St Homes, and Elevista. He started investing in 2011 after analyzing 1,100 deals and making zero offers, until a mentor handed him a pen and made him sign his first contract. Since then, Clark St has operated across single-family, multifamily, and land development, with Ed also invested as a limited partner in 1,000+ unit multifamily projects. Before real estate, he spent 24 years building systems for global companies in Silicon Valley. He hosts the Real Estate Underground podcast.